How New Trade Policies and Bond Market Shifts are Reshaping Housing in 2025

In 2025, Americans are navigating a housing market under pressure from two powerful forces: trade policy and inflation. Tariff expansions have driven up the cost of critical building materials, and immigration crackdowns are intensifying labor shortages in construction. Together, they’re pushing home affordability further out of reach for millions.

This post builds on my earlier article, How Proposed Policies Could Impact the Housing Market in 2025 and Beyond, where I outlined how these proposals — then still on the drawing board — could reshape the housing market. Today, those policies are in effect, and the results are unfolding much as anticipated.

1. Tariffs in Action — What’s Been Enacted

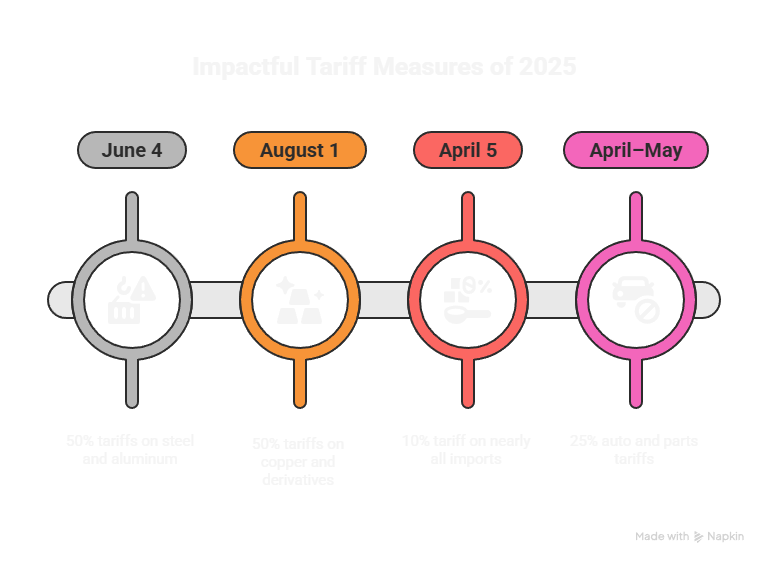

Since early 2025, the administration enacted sweeping tariff measures:

- 50% tariffs on steel and aluminum (June 4): U.S. imports of these materials represent over 30 million metric tons annually, used in framing, roofing, hardware, and appliances. This move raised domestic steel futures by roughly 25% since spring.

- 50% tariffs on copper and derivatives (August 1): Copper rod prices jumped 20–30%, directly affecting wiring, plumbing, and HVAC budgets.

- 10% tariff on nearly all imports (April 5): Affecting items from drywall to light fixtures. Tariff-weighted goods CPI is now ~3% higher than February baselines.

- 25% auto and parts tariffs (April–May): Ripple effects hit appliance imports that use similar manufacturing processes.

- Softwood lumber tariffs: At 14.5%, with a potential increase to 34.5%; U.S. imports from Canada totalled 25 billion board-feet last year, crucial for framing new homes.

In my prior article, I warned that such tariffs could add thousands of dollars to home costs — with double-digit percentage gains in steel, copper, and lumber, those warnings have proven accurate.

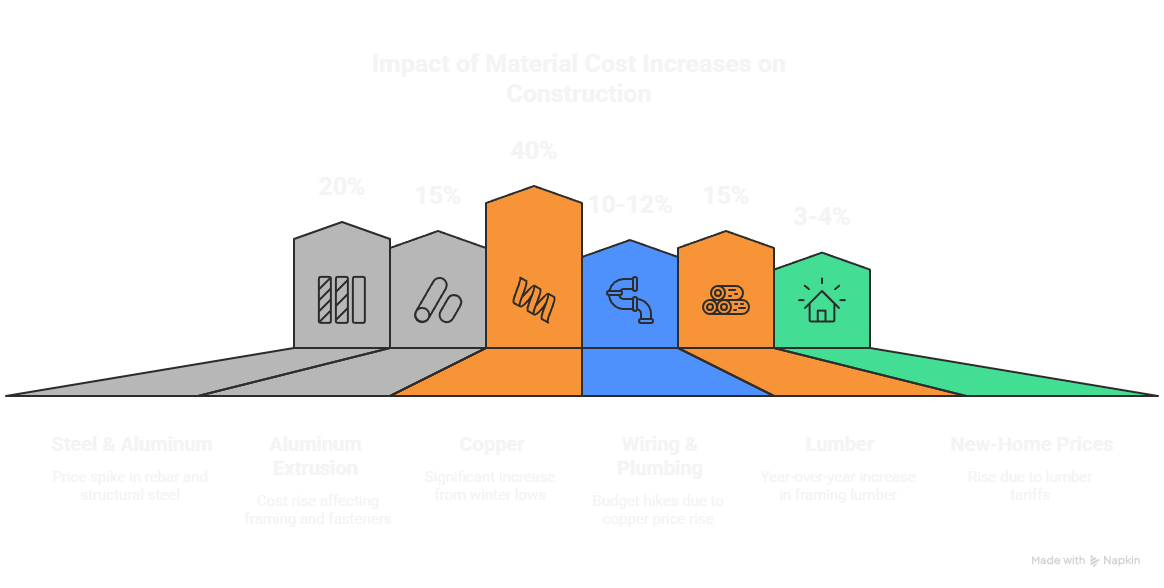

2. Building Materials Cost Surge

- Steel & Aluminum: Since June, spot prices for rebar and structural steel have spiked 20%, aluminum extrusion costs climbed 15% — feeding into framing, fasteners, gutters, and garage doors.

- Copper: Up nearly 40% from winter lows, driving 10–12% hikes in wiring and plumbing assembly budgets.

- Lumber: Framing-grade lumber is 15% more expensive year-over-year; NAHB estimates tariffs add $10,900 per home, raising new-home prices by 3–4%.

Smaller, regional builders — often providers of affordable housing — are most at risk, with many unable to absorb such cost shocks.

3. Labor Force Squeeze

As noted in my previous post on proposed policies, deportations threaten a key slice of the housing labor force:

- Immigrant workers account for 24% of U.S. construction labor; 13% of those are undocumented.

- With 400,000 unfilled positions pre-2025, losing even one-quarter of immigrant labor could drive construction wages up by 10–15%, particularly in labor-intensive trades like drywall, roofing, and concrete.

- Delays are mounting: some medium-sized builders report project timelines extending by 4–6 weeks, meaning delayed move-ins, lower turnover, and tighter supply pipeline.

- Higher labor, material, and regulatory costs cumulatively piggyback to deter new starts — pushing housing starts closer to historic lows.

4. Why the Fed Isn’t Cutting Aggressively

Mortgage rates follow the 10-year Treasury yield plus a risk spread — and that spread is currently elevated at ~2.3% (historic average ~1.75%).

The July PPI rose 0.9% m/m (+3.3% y/y), with much driven by goods costs — including tariff-affected inputs. Cutting aggressively now risks validating inflation expectations and pushing yields higher. The Fed is instead signaling smaller, measured cuts, aiming to avoid reigniting price pressures.

5. U.S. vs. Other Major Economies

- U.S. inflation: ~4% mid-2025 vs Eurozone ~2.5%, Japan ~1%, UK ~3.5%.

- Goods inflation: ~5.5% in the U.S. vs ~2–3% abroad, with tariffs a key driver.

- Many peer economies have begun gradual rate cuts; the Fed remains cautious due to higher domestic inflation and elevated bond term premiums.

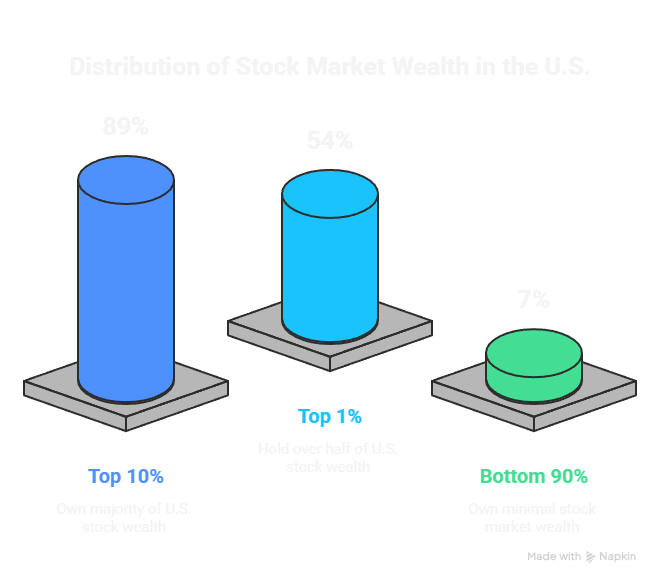

6. Stock Market ≠ Economic Health

While the stock market is holding up:

- Top 10% of households own ~89% of all U.S. stock wealth; the top 1% alone hold 54%.

- Gains don’t translate into affordability relief for most Americans.

- The S&P 500 can hit records while housing affordability hits lows — these metrics are not linked for the median household.

7. Affordability Compression

- Mortgage rates: 6.5–7%, double pre-pandemic levels.

- Materials costs: Up 10–25% depending on category (copper +40%, steel +20%).

- Labor costs: Rising 10–15% in many regions.

- Combined effect: Home prices rising 3–5% and mortgage payments up 20–30% for the same loan amount.

8. What to Watch

- 10-year Treasury yield — A 0.25% drop can shave ~0.25–0.50% off mortgage rates.

- Mortgage–Treasury spread — Falling from 2.3% toward 1.8% would offer relief even without yield drops.

- Tariff updates — Exemptions or rollbacks could lower costs in weeks.

- Construction labor data — Wage trends and workforce size will impact build rates.