How geopolitical conflict, rising energy costs, and inflation pressure could reshape the housing market heading into peak season

You might not think a military conflict thousands of miles away has anything to do with your plans to buy or sell a home. But if you’ve been watching gas prices creep up or hearing the words “inflation” and “mortgage rates” in the same sentence again — it’s all connected.

Right now, tensions between the United States and Iran have put a global spotlight on the Strait of Hormuz, a narrow waterway in the Middle East through which roughly 20% of the world’s oil supply passes every day. That’s about 20 million barrels. If that flow gets disrupted — even temporarily — the ripple effects don’t stop at the gas station. They reach into grocery stores, utility bills, construction sites, and yes, the housing market.

Oil has already climbed above $100 a barrel in recent weeks, a roughly 40% jump from pre-crisis levels. Mortgage rates, which had started to drift down into the high-5% range earlier this year, have climbed back above 6%. And all of this is happening right as we head into the spring and summer — traditionally the busiest time of year for real estate.

If you’re thinking about buying or selling a home in 2026, this is worth understanding. Not because you need to become an oil market expert, but because the forces driving energy prices are the same ones that will shape what you pay for a mortgage, what you can afford, and how active your local housing market will be over the next several months.

Let’s break it down.

Why a Conflict Halfway Around the World Could Affect Your Housing Plans

The Strait of Hormuz is essentially a 21-mile-wide bottleneck connecting the Persian Gulf to the rest of the world. Countries like Saudi Arabia, Iraq, the UAE, and Kuwait all ship their oil through it. When that passage is threatened — whether by military action, mines, or naval blockades — global oil markets react immediately.

We’re seeing that reaction right now. Crude oil prices have surged, and energy analysts warn that if the strait were partially or fully blocked for an extended period, oil could climb to $120, $140, or even higher. The International Energy Agency has warned that a full blockage could create the largest oil supply disruption in history.

For most Americans, this translates into one very visible and immediate cost: gasoline. But the less obvious — and arguably bigger — impact is what happens to inflation, interest rates, and the broader economy.

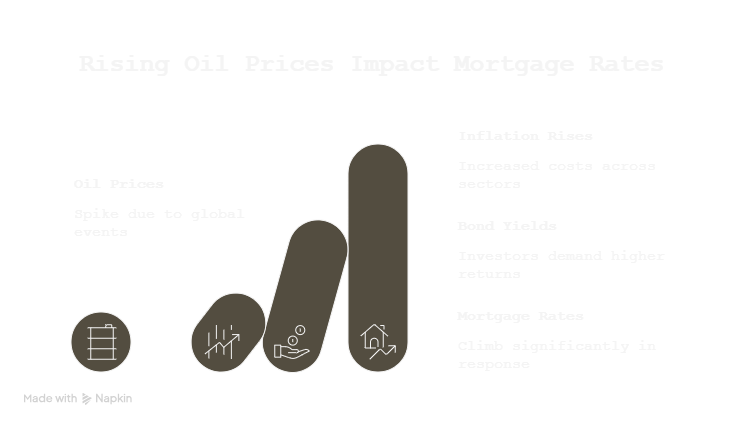

Why Oil Prices Matter to Mortgage Rates

If you’ve been following my work, you may remember an earlier post where I broke down how mortgage rates are actually determined. The short version: mortgage rates don’t follow the Federal Reserve’s rate directly. They follow the bond market, specifically the yield on the 10-year Treasury bond. And what drives those yields? Inflation expectations.

Here’s the chain reaction:

Oil prices rise → Transportation, heating, and manufacturing costs go up → Inflation rises → Bond investors demand higher yields to compensate → Mortgage rates climb.

When oil prices spike, it doesn’t just hurt at the pump — it raises the cost of moving goods, heating homes, generating electricity, and producing food. All of that feeds into the inflation numbers the Federal Reserve is watching. And when inflation runs hot, the Fed either raises interest rates or holds them higher for longer to bring prices back under control.

That’s exactly what happened in 2022 when Russia invaded Ukraine. Oil surged past $120 a barrel, gas hit $5 a gallon nationally, and inflation hit 9.1% — a 40-year high. The Fed responded with the most aggressive rate hikes in decades. Mortgage rates doubled from about 3.3% to over 7% in less than a year. The housing market went from red-hot to frozen.

Goldman Sachs has estimated that if oil averages around $98 a barrel over the coming months due to the current Iran situation, U.S. inflation could jump by roughly 0.8 percentage points and GDP growth could take a 0.3-point hit. That may sound small, but in a market where buyers are already stretched thin, even a modest rate increase has a big impact on affordability.

As I’ve noted in previous posts, roughly a 1 percentage point increase in mortgage rates reduces a buyer’s purchasing power by about 10%. That’s not abstract — it’s the difference between qualifying for a $300,000 home and being limited to $270,000.

How Higher Energy Costs Squeeze Buyers and Sellers

When gas prices jump, the impact goes well beyond your weekly fill-up. Rising oil prices act like an invisible tax on almost everything:

Your daily budget takes a hit. If you’re suddenly spending $200 more per month on gas and utilities, that’s $200 less you have for a mortgage payment, savings, or a down payment. For buyers already navigating an affordability crisis — where the average first-time buyer is now nearly 40 years old and first-time buyers represent just 21% of the market — any additional squeeze on the household budget can be the difference between buying and waiting.

Consumer confidence drops. Homebuying is one of the most confidence-dependent decisions a person can make. When gas prices are climbing, grocery bills are rising, and headlines are filled with talk of conflict and economic uncertainty, even financially qualified buyers tend to pull back. They wait. They second-guess. And that hesitation slows the entire market.

Construction costs rise. Diesel fuel powers the heavy equipment that builds homes. Petroleum-based products — asphalt shingles, PVC pipes, synthetic carpeting, insulation — are embedded in nearly every stage of construction. When oil prices spike, builders face higher costs for materials and transportation, which either get passed on to buyers in the form of higher prices, or cause builders to delay or cancel projects altogether. As I covered in my post on tariffs and housing, rising material and input costs were already adding thousands of dollars to new home prices. An oil shock layers more pressure on top of that.

Commuting costs reshape demand. When gas is $4 or $5 a gallon, that long suburban commute gets a lot more expensive. Homes farther from job centers can lose some of their appeal, while properties closer to work or near public transit may gain relative value. For a market like greater Nashville — where many residents commute by car — sustained high fuel prices can meaningfully affect which neighborhoods stay hot and which cool off.

What History Tells Us: Past Oil Shocks and the Housing Market

This isn’t the first time an oil crisis has shaken the housing market. And the historical pattern is remarkably consistent: oil prices spike, inflation follows, the Fed tightens, and the housing market slows. Let’s look at a few key examples.

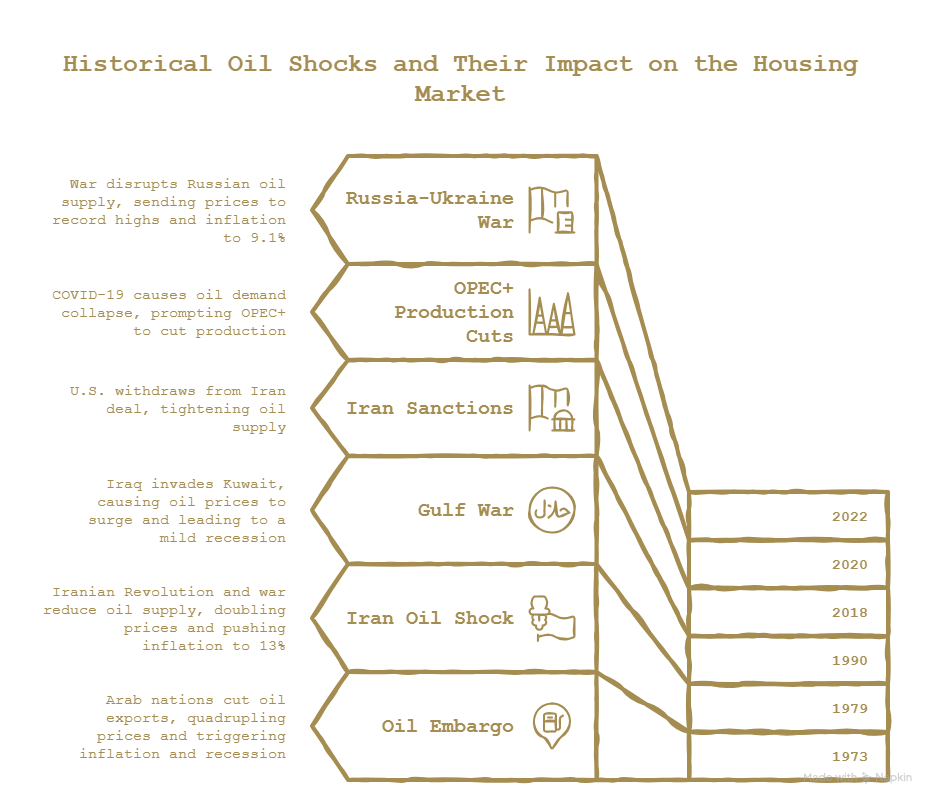

The 1973 Oil Embargo

When Arab oil-producing nations cut off exports to the U.S. in response to the Yom Kippur War, oil prices quadrupled from about $3 to $12 a barrel. Gasoline prices jumped 43%. Inflation soared into double digits, and the 1973–75 recession hit hard — GDP contracted and unemployment eventually peaked at 9%.

Mortgage rates climbed toward 9–10% by 1974. Home sales slowed, consumer confidence cratered, and builders pulled back as fuel and material costs surged. The term “stagflation” — high inflation combined with slow growth — entered everyday vocabulary for the first time.

The 1979 Iran Oil Shock

The Iranian Revolution and the Iran–Iraq War took another massive chunk of oil off the global market. Oil prices roughly doubled again, reaching about $36 a barrel by 1980. U.S. inflation hit approximately 13%.

Fed Chairman Paul Volcker responded with aggressive rate hikes that pushed mortgage rates above 18% by 1981 — the highest in American history. The housing market effectively collapsed under those financing costs. Home sales and construction plummeted. It took years for the market to recover, and the early 1980s remain the most extreme example of how an oil shock can devastate housing affordability.

The 1990 Gulf War

Iraq’s invasion of Kuwait in August 1990 caused oil prices to surge 135% in a matter of weeks. Gasoline and heating costs jumped, pushing inflation above 6%. Mortgage rates hovered around 10%, and the mild 1990–91 recession followed.

The housing market “slugged along for years” as consumer optimism evaporated. Many would-be buyers retreated, and sellers had to temper expectations. Once the war ended quickly and oil prices receded, the Fed cut rates and the market gradually recovered — but not before several quarters of lost momentum.

The 2022 Russia-Ukraine Energy Shock

This one is still fresh — but the full story starts a few years earlier.

In May 2018, the Trump administration withdrew the United States from the Iran nuclear deal (the JCPOA) and reimposed sanctions targeting Iran’s energy sector. That move effectively pulled a significant chunk of Iranian oil off the global market, tightening supply.

Then in April 2020, when COVID-19 caused oil demand to collapse and prices briefly went negative, the Trump administration brokered a historic deal with OPEC+ — including Russia and Saudi Arabia — to cut global oil production by 9.7 million barrels per day. At the time, the cuts were seen as necessary to stabilize a crashing market and protect the U.S. oil industry from a wave of bankruptcies. But those production cuts were only unwound gradually over the next two years, which meant that by the time global demand came roaring back in 2021, supply was still playing catch-up.

So when Russia invaded Ukraine in February 2022, the global oil market was already tight. The war sent crude above $120 a barrel and U.S. gasoline to a record $5-plus per gallon. The combination of sanctions on Iranian oil, lingering OPEC+ production cuts, and the sudden loss of Russian supply created a perfect storm. Inflation hit 9.1% — a 40-year high.

The Fed responded with the most aggressive rate hikes in decades. Mortgage rates doubled from about 3.3% to over 7% in less than a year. Home sales dropped about 30% year-over-year. Consumer sentiment hit its lowest point on record.

The housing market went from bidding wars and waived inspections to price cuts and longer days on market — almost overnight. Markets like Austin and Phoenix saw price corrections. Nationally, the spring 2022 selling season was effectively canceled by the combination of inflation and rising rates.

The 2022 episode is a reminder that oil shocks rarely come from a single cause. Policy decisions made years earlier — regardless of which administration makes them — can shape how vulnerable the market is when the next disruption hits. The Iran sanctions, the OPEC+ cuts, and the war in Ukraine each played a role. And that layered dynamic is worth keeping in mind as we watch the current situation unfold.

The Common Thread

In every case, the sequence is the same: oil shock → inflation → higher interest rates → weaker housing demand. The severity depends on how long the disruption lasts and how aggressively policymakers respond. Short-lived shocks (like the 1990 Gulf War) cause temporary slowdowns. Prolonged crises (like the late 1970s) can reshape the market for years.

What This Could Mean for Homebuyers

If you’re planning to buy a home in 2026, here’s how this situation could affect you:

Mortgage rates may stay elevated longer than expected. Earlier this year, many forecasters expected rates to gradually drift lower. That outlook is now in question. If oil-driven inflation persists, the Fed may hold rates steady or even signal further tightening — which would keep mortgage rates in the 6%-plus range or push them higher. As I discussed in my post on mortgage rate mechanics, what matters most isn’t what the Fed does with its overnight rate — it’s what happens to inflation expectations and Treasury yields.

Your purchasing power could shrink. Between potentially higher mortgage rates and increased costs for gas, groceries, and utilities, the amount you can comfortably spend on a home may be less than you planned. It’s worth running your budget numbers with a rate that’s 0.5% to 1% higher than today’s quotes, just to give yourself a cushion.

Less competition could work in your favor. A slower market means fewer bidding wars and more negotiating room. If other buyers pull back due to uncertainty, well-prepared buyers may actually find better opportunities. Some sellers may offer concessions like rate buydowns to attract buyers — which can make a meaningful difference in your monthly payment.

Think about long-term costs, not just the purchase price. In an era of expensive energy, a home’s efficiency matters more. Look at insulation, HVAC age, window quality, and even solar panels. A shorter commute can save you hundreds per month if gas stays at $4 or $5. These factors can offset some of the affordability pressure from higher rates.

What This Could Mean for Sellers

Your buyer pool may be smaller. If rates stay elevated and household budgets are squeezed by higher energy costs, fewer buyers will qualify at your asking price. This is especially true in the middle price tiers where buyers are most rate-sensitive.

Pricing realistically is more important than ever. In a market where buyers are cautious and affordability is tight, overpricing is the fastest way to watch your home sit. The homes that sell are the ones priced for today’s market, not last year’s.

Consider offering buyer incentives. Helping a buyer with closing costs or offering a temporary rate buydown (where you subsidize a lower rate for the first year or two) can make your home more attractive without cutting your price. In a volatile rate environment, these strategies can be powerful differentiators.

If you’re planning to sell, sooner may be better than later. If the geopolitical situation worsens and economic conditions tighten further, buyer demand could soften heading into summer and fall. Listing during the early spring window, while there’s still market activity, may give you the best audience.

What Buyers and Sellers Should Watch Right Now

This section is your checklist for the coming months. You don’t need to track every economic indicator — but keeping an eye on these key signals will help you make smarter decisions:

Mortgage rates. Check weekly. If rates are drifting up, it signals that inflation fears are growing. If they’re stable or declining, the market may be absorbing the oil shock without major damage.

Inflation reports (CPI). The Consumer Price Index, released monthly, is the number the Fed watches most closely. If headline inflation starts rising again — especially if “core” inflation (which excludes food and energy) also ticks up — expect the Fed to stay hawkish and rates to remain firm.

Gas prices. This is your most visible, real-time indicator. National averages above $4 suggest sustained pressure. Above $5 means the economy is under real strain.

Consumer confidence surveys. The University of Michigan Consumer Sentiment Index is a good barometer. When confidence drops, housing demand typically follows within a few months.

Housing inventory and days on market. Watch your local market. If homes are sitting longer and inventory is growing, it’s a signal that buyers are pulling back. If inventory stays tight, that’s a floor under prices even in a slowing market.

The 10-year Treasury yield. As I’ve explained before, this is the benchmark that most directly influences mortgage rates. If the 10-year yield is rising, mortgage rates will follow. A drop in yields would signal some relief ahead.

Local job market conditions. Are employers in your area hiring or laying off? In a metro like Nashville, the strength of the healthcare, music/entertainment, and tech sectors matters. A strong local economy can buffer against national headwinds.

A Quick Note for the Nashville and Middle Tennessee Market

Nashville doesn’t have an oil industry to cushion the blow the way Houston or Midland, Texas might. When oil prices spike, it’s a pure cost increase for Middle Tennessee households — higher gas, higher utility bills, higher grocery prices — with no local economic upside to offset it.

At the same time, Nashville’s housing market has seen significant price appreciation in recent years, and inventory remains relatively tight. That combination — elevated home prices plus rising costs of living — puts additional pressure on buyers who are already stretched. As I discussed in my posts on wealth inequality and housing affordability and policy promises vs. market reality, the structural challenges facing buyers in markets like Nashville run deep. An oil shock doesn’t create those problems, but it amplifies them.

The good news is that Nashville continues to attract population growth, job creation, and investment. That underlying demand provides a floor that many other markets don’t have. But buyers here should budget conservatively, and sellers should price with an awareness that today’s buyer is more cautious and more cost-conscious than the buyer of 2021 or 2022.

Conclusion: Stay Informed, Stay Prepared, Don’t Panic

Oil price shocks are disruptive, but they’re not permanent. Every historical episode we’ve looked at — from the 1973 embargo to the 2022 Russia-Ukraine spike — eventually resolved. Inflation came down, rates adjusted, and the housing market found its footing.

That doesn’t mean the next several months will be easy. If the Iran situation escalates and oil prices stay elevated, we’re likely looking at a spring and summer market that’s more sluggish than many people hoped for. Mortgage rates may stay stubbornly high. Affordability will remain a challenge. And the buyers and sellers who come out ahead will be the ones who understand what’s driving the market and plan accordingly.

Throughout my writing on this blog, I’ve tried to make one thing clear: the housing market doesn’t exist in a vacuum. It’s shaped by Federal Reserve policy, inflation, bond markets, trade policy, wages, construction costs, and yes — what’s happening in the oil markets half a world away. The more you understand those connections, the better equipped you are to make smart, confident real estate decisions.

If you’re a buyer, build some cushion into your budget. Get pre-approved. Lock your rate when it makes sense. Don’t stretch beyond what’s comfortable even in the best-case scenario.

If you’re a seller, price for the market you’re in, not the one you wish you were in. Be open to creative deals. And if you’ve been thinking about listing, don’t wait for perfect conditions — they may not arrive this year.

And whether you’re buying, selling, or just watching from the sidelines — stay informed. The situation is evolving, and the decisions you make in the next few months will be better for understanding the bigger picture.

As always, feel free to reach out with questions. I’m here to help you navigate whatever the market throws our way.

Sources: Federal Reserve History, Chicago Fed Letter, Freddie Mac Multifamily Research, Los Angeles Times/AP, Zillow Research, Realtor.com News, Axios Economy, ConstructConnect News, ABC News/Forbes