How Decades of Policy Decisions and Economic Shifts Have Reshaped the Path to Homeownership for a New Generation

Owning a home has long been considered a cornerstone of the American Dream. However, for younger generations, this dream is slipping further out of reach. A combination of wealth inequality, wage stagnation, and policies dating back to the Nixon and Reagan administrations have reshaped the economic landscape, leaving many young people struggling to achieve financial independence and homeownership. This blog dives into the historical roots of these issues, their lasting effects, and what this means for the housing market today.

Key Historical Context: Nixon and Reagan Administrations

The economic shifts that paved the way for today’s wealth inequality and wage stagnation began in the 1970s and 1980s. Policies during the Nixon and Reagan administrations played a pivotal role:

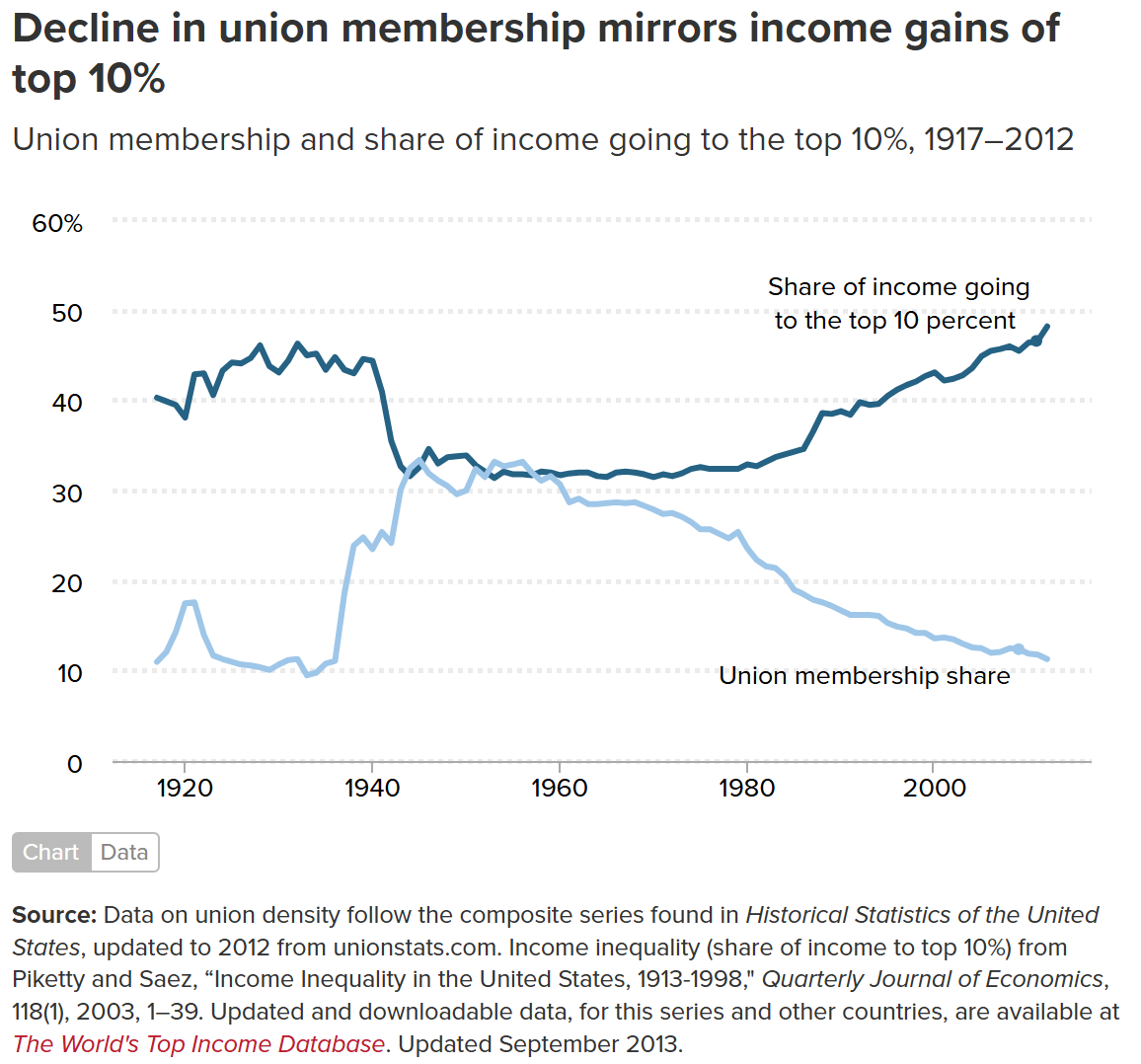

The Decline of Unions

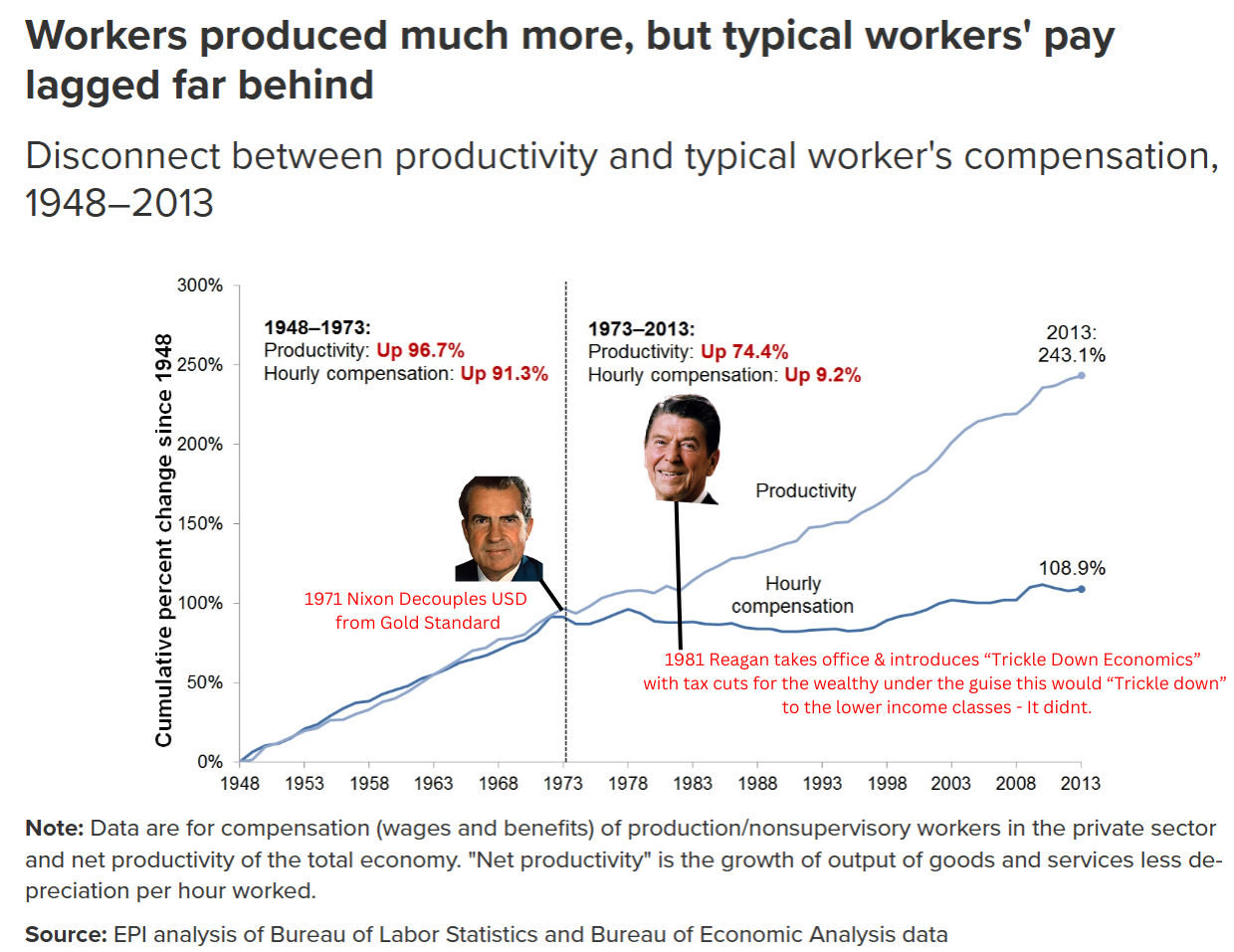

In 1971, President Nixon ended the Bretton Woods system by taking the U.S. off the gold standard, leading to higher inflation and economic instability. This created pressure on unions, which had historically negotiated strong wage growth for workers.

The Reagan administration intensified the decline of unions by dismantling their power. A key event was the 1981 air traffic controllers’ strike (PATCO), where Reagan fired over 11,000 striking workers, setting a precedent for union-busting.

Policies such as deregulation and tax cuts for corporations further weakened collective bargaining power, leading to stagnation in wages.

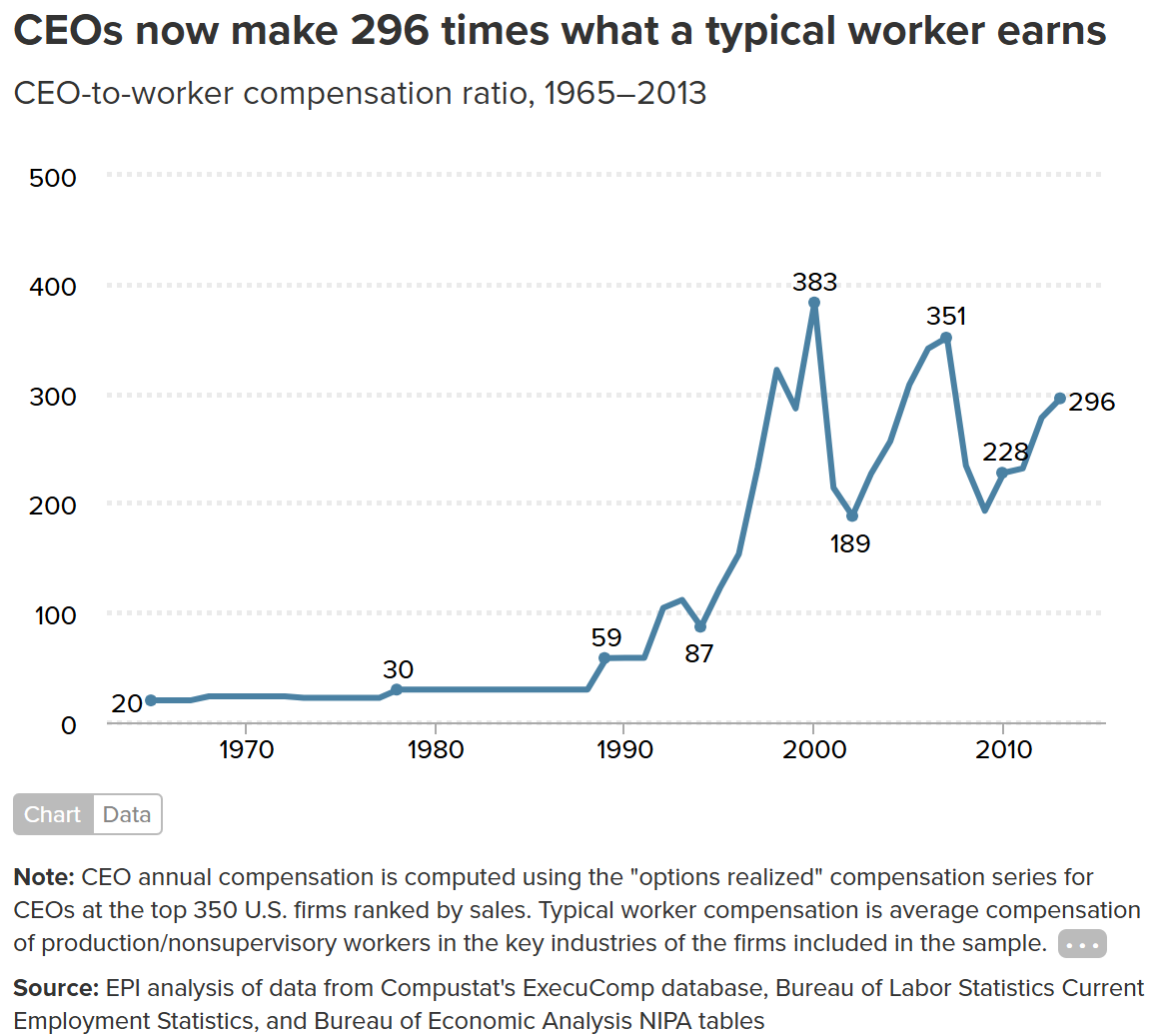

A more recent example includes the 2017 Tax Cuts and Jobs Act, which promised benefits for workers but largely resulted in record-breaking stock buybacks and stock market gains. This is significant because the stock market is disproportionately owned by the wealthiest Americans, with the top 10% owning approximately 89% of all stocks, according to Federal Reserve data. This dynamic further widened the gap between corporate profitability and worker compensation, leaving the working class with little to show for these policies.

Supply-Side Economics (Trickle-Down Theory)

Reagan’s economic policies, known as “Reaganomics,” or “Trickle Down Economics,” emphasized tax cuts for the wealthy and corporations, under the belief that benefits would “trickle down” to workers.

While corporate profits soared, wages for middle- and lower-income workers stagnated, exacerbating wealth inequality.

Globalization and Outsourcing

Both administrations promoted free trade agreements that led to the outsourcing of manufacturing jobs. This eroded the economic stability of working-class Americans, who once relied on these jobs to build wealth and achieve homeownership.

More recently, the use of H1B visas has sparked debate as company executives increasingly promote hiring foreign visa holders as a cost-saving measure over employing qualified American workers. Critics argue that this practice prioritizes profitability over fair wages for domestic employees, further contributing to wage stagnation and limiting economic opportunities for American workers.

The Wage Stagnation Crisis

Since the 1970s, wages for most workers have remained flat, even as productivity has increased significantly. This divergence is a critical factor in the erosion of homeownership opportunities for young people.

Key Data Points

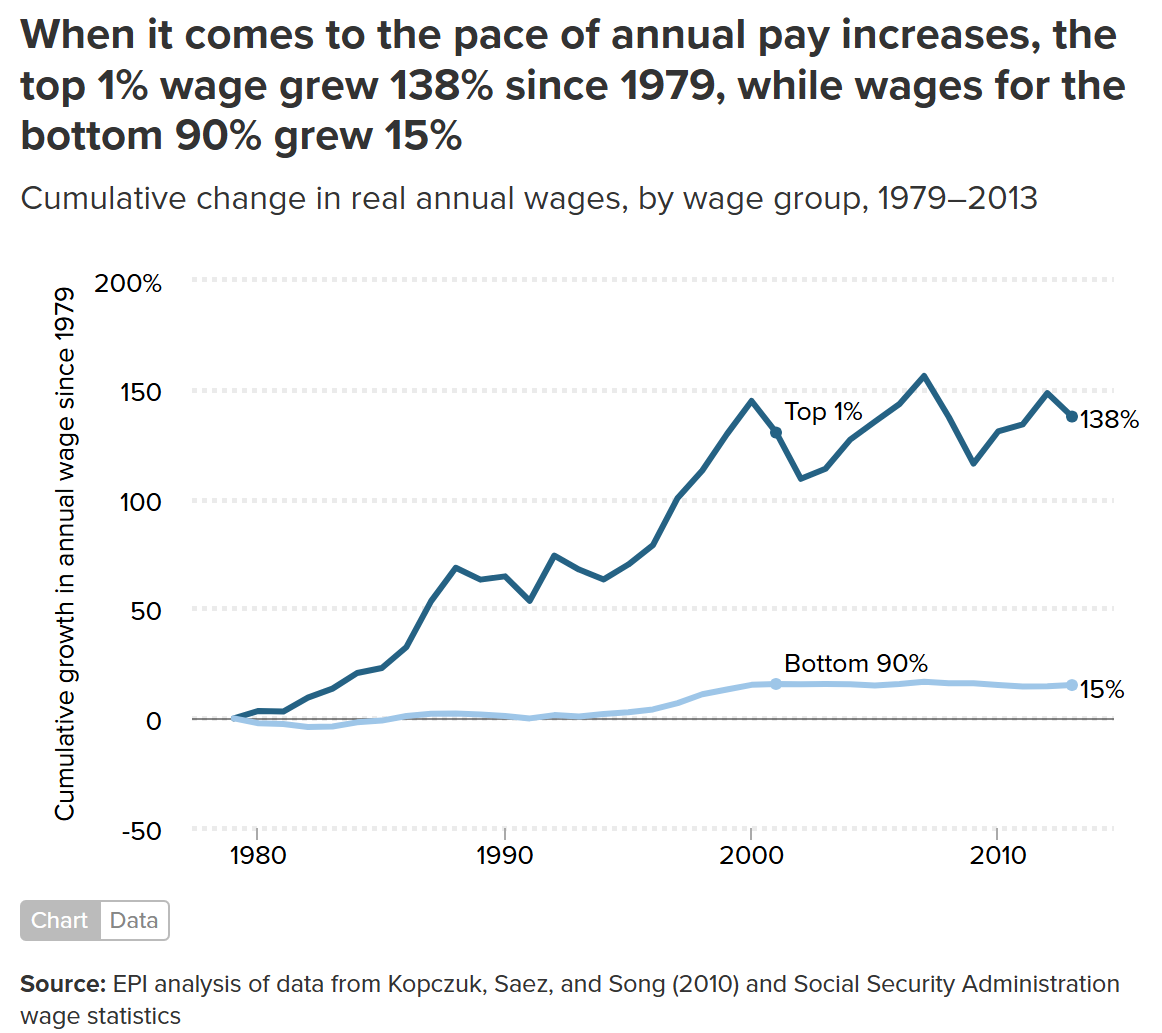

Wage Growth vs. Productivity: According to the Economic Policy Institute (EPI), from 1979 to 2020, productivity grew by 61.8%, while hourly pay grew by only 17.5%.

Minimum Wage Stagnation: The federal minimum wage, adjusted for inflation, peaked in 1968. Since then, its purchasing power has declined by over 30%. The original intent of the minimum wage was to ensure that workers could maintain a livable standard of living, providing a baseline threshold for economic security. However, in the pursuit of corporate profitability, this foundational principle has been eroded. Today, many minimum wage jobs fail to support even basic living expenses, highlighting how prioritizing profits has come at the expense of the American working class.

Critics of raising the minimum wage often argue that it would lead to upward pressure on the pricing of everyday necessities. However, even with the current historically low minimum wage, prices for goods and services have skyrocketed due to inflation and record corporate profitability. Many corporations have prioritized stock buybacks, enriching executives and wealthy shareholders, while wages for workers have remained stagnant. This dynamic underscores how rising prices are not necessarily tied to higher wages but rather to corporate decisions that prioritize profits over fair compensation for labor.

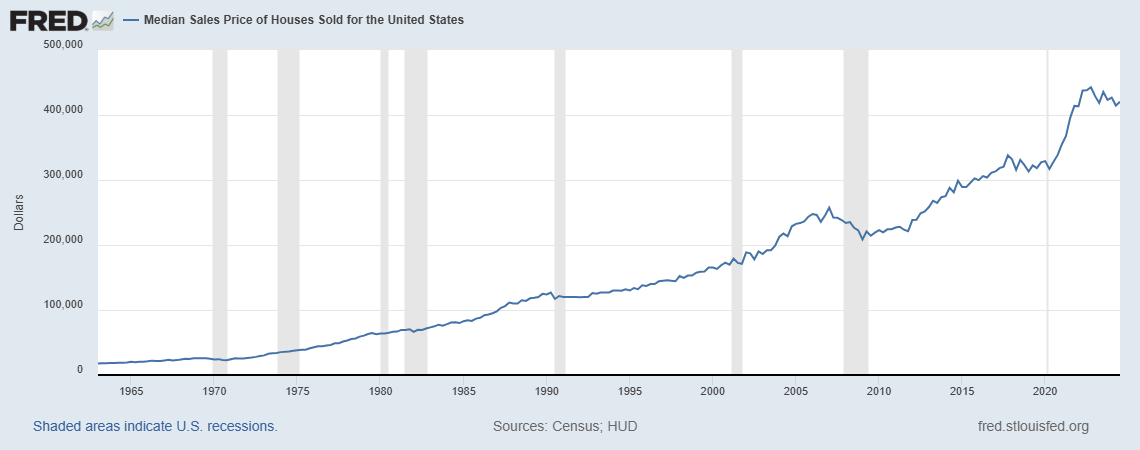

Housing Price Growth: Meanwhile, the median home price has increased by 121% from 1960 to 2020, far outpacing wage growth.

Wealth Disparity and Its Impacts

Historical Wealth Trends

The distribution of wealth in the U.S. has shifted dramatically since the 1970s. Economic policies during this period favored the wealthy, leading to a concentration of assets among the top earners.

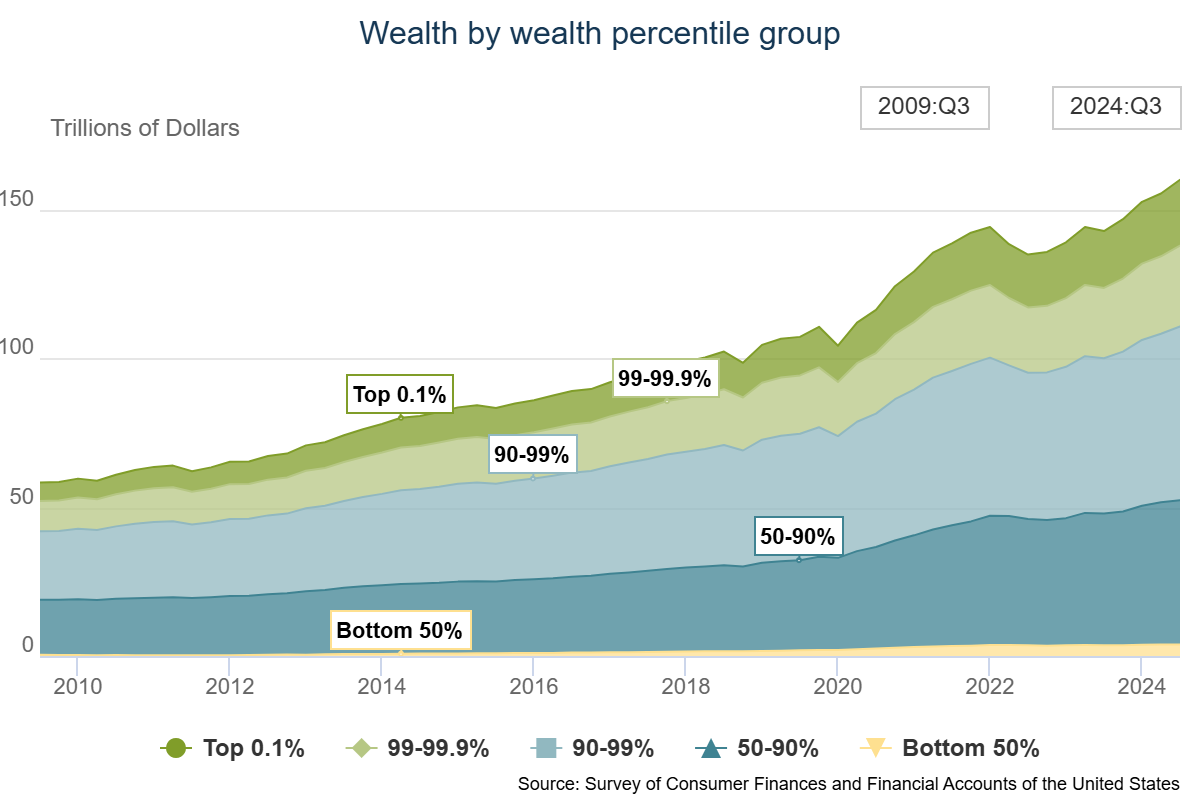

- 1970s: The top 10% of earners controlled approximately 60% of the nation’s wealth, while the bottom 50% held around 20%.

- 2020s: Today, the top 10% control nearly 80% of the wealth, while the bottom 50% hold less than 10%, according to Federal Reserve data.

Contributing Policies

Tax Cuts for the Wealthy:

Reagan’s 1981 Economic Recovery Tax Act significantly reduced top marginal tax rates, benefiting the wealthiest Americans. Over subsequent decades, additional tax policies continued to favor high-income earners, exacerbating wealth concentration.

Erosion of Social Safety Nets:

Cuts to public assistance programs began in earnest during the Reagan administration, with a focus on reducing federal spending on welfare and other safety net programs. Initiatives like the 1981 Omnibus Budget Reconciliation Act reduced funding for programs such as food stamps, Medicaid, and housing assistance.

These cuts were motivated by a belief in smaller government and a desire to encourage self-reliance. However, critics argue that these reductions disproportionately affected lower-income families, limiting their upward mobility and contributing to the widening wealth gap.

Education funding cuts during this time also widened the wealth gap by limiting access to quality education for working-class Americans. These cuts reduced funding for public schools and state universities, leading to higher tuition costs and less accessible higher education. The diminished support for affordable education forced many young people to take on significant student loan debt, which remains a critical barrier to homeownership today. According to the Federal Reserve, the average student loan borrower owes over $30,000, delaying their ability to save for a down payment and qualify for a mortgage. This cycle has entrenched generational disparities, with education — once a pathway to upward mobility — becoming a source of financial strain.

Asset Appreciation:

Wealthier individuals invested in assets such as real estate and stocks, which appreciated significantly over time. Lower-income families, lacking disposable income for investments, missed out on this wealth-building opportunity.

Impact on Younger Generations

- Reduced Savings: With wages stagnating and costs for essentials rising, younger people struggle to save for a down payment.

- Increased Debt: High levels of student loan debt and credit card debt make it difficult to qualify for mortgages.

- Generational Wealth Transfer: The lack of inherited wealth further widens the gap, as younger generations do not have access to the same financial safety nets as previous ones.

How Wealth Inequality Shapes the Housing Market

Rising Home Prices:

Concentrated wealth has allowed investors and corporations to buy up properties, driving prices higher and reducing inventory for first-time homebuyers.

Institutional ownership of single-family homes has significantly impacted housing affordability in metro areas like Atlanta. In the fourth quarter of 2021, investors accounted for approximately 41% of all home sales in Atlanta, illustrating their dominance in the market. This trend has driven median home prices in the area up by over 108% in just two years, putting homeownership further out of reach for many.

Nashville has also been heavily influenced by institutional investors. In the first quarter of 2022, nearly 30% of all homes sold in Nashville were purchased by investors, many of them institutional buyers. This has driven up prices, reduced available inventory for individual buyers, and converted a significant number of properties into rentals, further exacerbating affordability issues.

The Federal Reserve’s policies of low-interest rates have also inflated asset prices, including real estate, benefiting wealthier individuals with access to credit.

Generational Wealth Disparities:

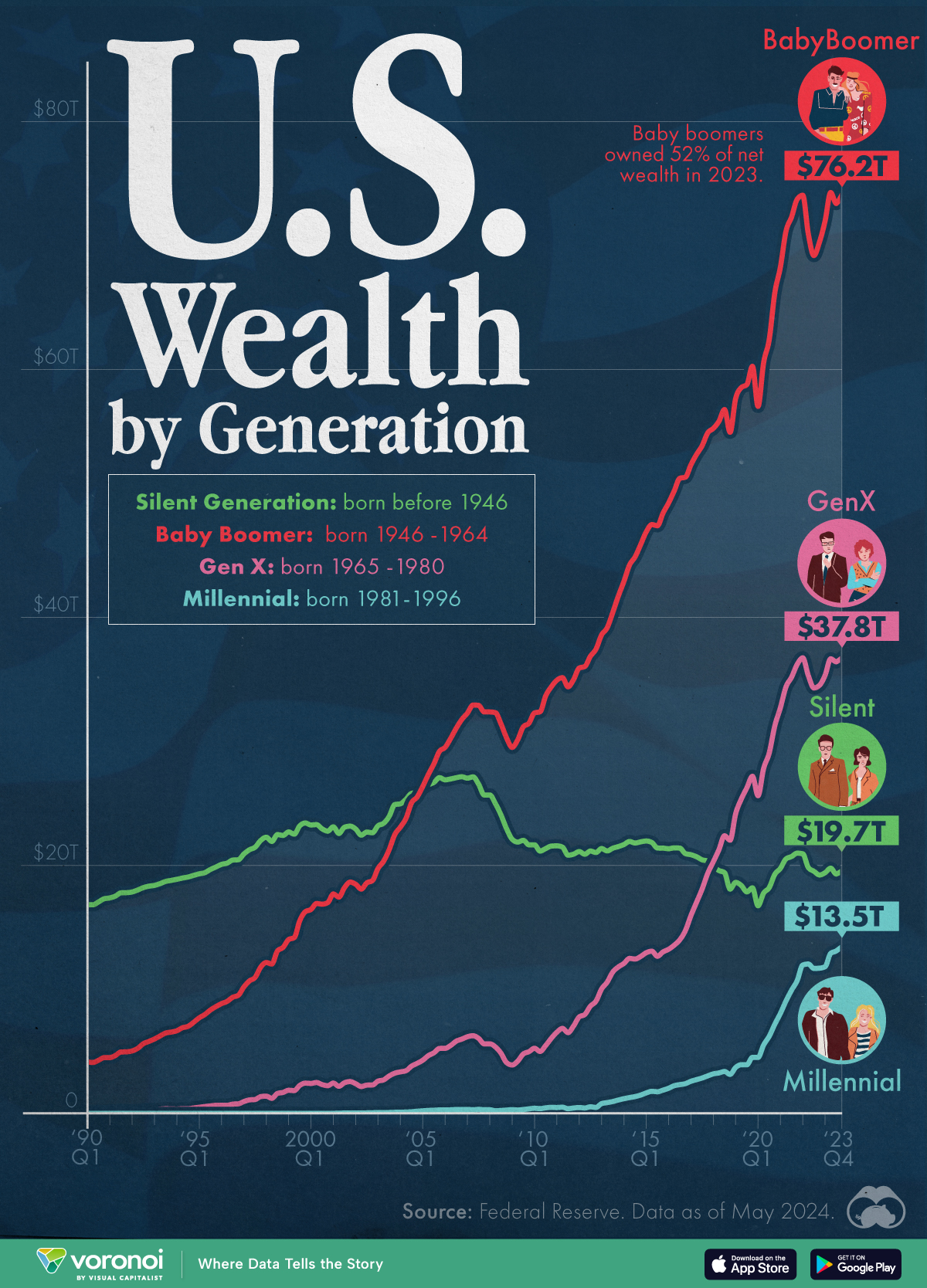

Baby Boomers hold over 50% of the nation’s wealth, while Millennials hold just 4.6% (there are now 40+ year old Millennials), according to the Federal Reserve. This disparity limits younger generations’ ability to afford homes.

Effects on Young Buyers Today

Delayed Homeownership: The homeownership rate for Millennials is 8% lower than that of Gen X and Baby Boomers at the same age, per a 2020 report by the Urban Institute.

Shift to Renting: With home prices surging, many young people are renting longer, often spending over 30% of their income on rent, leaving little room to save for a down payment. Financial experts recommend spending no more than 30% of one’s income on housing to maintain a balanced budget. However, the reality is starkly different for most renters today. According to recent studies, nearly half of renters spend more than 30% of their income on housing costs, and one in four spends over 50%. This burden further delays savings for a home purchase, locking many young people into a cycle of renting without viable paths to ownership.

Geographic Constraints: Affordability has pushed younger buyers to relocate to less expensive markets, often far from job opportunities and family support systems.

Increasing Age of First-Time Buyers: The average age of first-time homebuyers has increased to 38 years old, a significant rise compared to earlier decades. This trend is a direct reflection of the challenges discussed in this blog: wage stagnation, rising home prices, and the concentration of wealth. Policies favoring the wealthy have left younger generations with fewer resources to save for a home. Student loan debt and limited access to affordable housing exacerbate this issue, delaying homeownership and forcing many to rent for extended periods.

First-Time Homebuyer Participation Hits Record Low

According to the 2024 Profile of Home Buyers and Sellers by the National Association of Realtors (NAR), first-time homebuyers now represent just 24% of all buyers, marking the lowest share since the data collection began in 1981. This decline underscores how challenging it has become for first-time buyers to enter the market, as home prices near record highs and mortgage rates stay firmly above 7%.

Before the 2008 subprime mortgage crisis, first-time buyers typically made up around 40% of the market. The significant drop since then reflects how economic shifts, coupled with rising costs and stagnant wages, have relegated many potential buyers to the sidelines.

These data points provide a stark reminder of the systemic barriers facing first-time homebuyers today. Understanding these challenges is critical for crafting strategies to overcome them and successfully navigate the real estate market.

Conclusion

The intersection of wealth inequality and wage stagnation has created significant barriers to homeownership for young people. These challenges are deeply rooted in decades-old policies and systemic economic shifts, but bringing these issues to light is the first step toward meaningful change. By understanding the mechanisms that have led us here, from wage stagnation to the concentration of wealth and institutional ownership of homes, we can begin to address the inequities that hinder many from achieving financial independence and homeownership.

It is crucial to recognize the nuance in this situation. These barriers are not insurmountable, but they require collective awareness and action. Advocating for fair wage policies, affordable housing initiatives, and financial education can empower individuals and communities to push back against the trends that have made homeownership so difficult.

As we share these facts and insights, we help to build a more informed public, fostering conversations that lead to solutions. The American Dream of owning a home may seem out of reach for many today, but with persistent effort and systemic changes, we can ensure it remains a possibility for future generations. Let this knowledge inspire hope and action — because awareness is the foundation of progress.

Have any questions about how to interpret these charts and data? Questions in general? Reach out to me to see how understanding this information can empower you to make informed decisions in today’s housing market. I strive to educate my clients and anyone reading these posts, equipping them with tools that will help them succeed and reach their goals. Knowledge is power, and staying informed is the first step toward navigating the challenges and opportunities ahead.

Sources: Economic Policy Institute, Federal Reserve Bank of St. Louis, Bureau of Labor Statistics, Federal Reserve, Atlanta Civic Circle, Fox 17 Nashville, Local Housing Solutions, Visual Capitalist, MarketWatch, National Association of Realtors