Buying and selling at the same time can feel like trying to land two planes on the same runway. Here’s how I’d actually think about it for a Middle Tennessee move in 2026.

If you own a home in Middle Tennessee and you’re trying to move into your next one, you’re probably running into the same question I’m getting from move-up buyers, downsizers, and relocation clients almost every week:

Should I sell my current home first, buy the next one first, or try to do both at the same time?

You may want to buy the next home before someone else gets it. But you may also need the equity from your current home to make the numbers work. You might not want to move twice, but you also don’t want to carry two mortgage payments if your current home takes longer to sell than you expect.

So the question becomes: which risk are you better positioned to absorb?

The honest answer isn’t a one-size-fits-all rule. It depends on your finances, your current home, the home you want to buy, and the local market conditions where you’re moving. Here’s how I’d think about it for clients in White House, Portland, Gallatin, Hendersonville, Springfield, Goodlettsville, Greenbrier, Cottontown, and the surrounding north-of-Nashville markets.

The Market Backdrop Matters

This decision doesn’t happen in a vacuum. The current Middle Tennessee market is more balanced than the 2021–2022 frenzy, and that changes which strategy makes sense.

Greater Nashville REALTORS® has reported higher inventory and longer days on market across the region. As I covered in Should I Buy Now or Wait in Middle Tennessee?, the March 2026 report closed with 13,694 active listings — up roughly 11% year over year — while closings dipped only 3%. That’s the picture you should hold in your head as you weigh these options:

- More inventory means buyers have more choices and more negotiating room.

- Longer days on market means well-priced, well-prepared homes still sell, but overpriced ones sit.

- Sellers are increasingly open to concessions — closing-cost credits, repair credits, rate buydowns.

That backdrop opens up strategies that didn’t really exist during the frenzy years. A contingent offer that would have been thrown straight in the trash in 2021 can be a workable negotiation in 2026 — if the rest of your situation is strong.

Mortgage rates are still a factor too. Freddie Mac’s Primary Mortgage Market Survey put the average 30-year fixed-rate mortgage at 6.36% as of May 14, 2026. That number matters because it sets the monthly payment math on both sides of your move — including whether you can comfortably carry two homes if the timing slips.

Option 1: Sell First, Then Buy

Selling first is usually the safer financial route.

When you sell your current home before buying the next one, you know exactly how much equity you have available. The next purchase is cleaner — no contingencies, no guesswork, no pressure from a sale that hasn’t happened yet. For many downsizers and retirees, that clarity is the whole point.

The downside is the timing gap. You may need temporary housing, short-term storage, or a rent-back arrangement with the buyer of your current home. And once your sale closes, the clock starts ticking on finding the next place before your bridge plan runs out.

This strategy tends to work well when:

- You need your current home’s equity for the next down payment

- You don’t want to risk two mortgage payments

- You’re downsizing, retiring, or simplifying — and flexibility on timing is realistic

- You have family, a rental, or short-term housing available between closings

- Your next-home search isn’t extremely narrow

For many downsizers in White House, Hendersonville, Gallatin, and Portland, selling first creates the cleanest possible decision tree. You know your proceeds. You know your budget. You can make the next move with real numbers instead of estimates.

One overlooked option here: you can often negotiate a post-closing occupancy (a “rent-back”) with your buyer, giving you 30, 45, or 60 days in the home after closing to find and close on the next one. That’s a tool, not a guarantee — but in a more balanced market with motivated buyers, it’s worth asking about.

Option 2: Buy First, Then Sell

Buying first is more convenient, but it usually requires stronger finances.

This approach lets you move once, prepare your current home for sale after you’re out, and avoid temporary housing. It’s especially helpful if your current home needs cleaning, decluttering, paint touch-ups, or staging that’s hard to do while you’re still living in it.

The risk is obvious: if your current home doesn’t sell quickly, you’re carrying two mortgages, two utility bills, two insurance policies, two property tax bills, and ongoing maintenance on both. At a 6.36% rate environment, that’s not a small monthly hit.

This strategy tends to work well when:

- You can qualify for the next home without selling first (debt-to-income still works on both)

- You have enough cash or equity access for the down payment without your sale proceeds

- Your current home is genuinely marketable — priced right, presented well, in a desirable location

- You have a realistic backup plan if the sale takes longer than expected

- You’re comfortable — emotionally and financially — carrying two properties for a few months

One thing worth flagging: bridge financing and HELOCs. Some buyers tap a home equity line of credit on the current home to cover the down payment on the next one, then pay it back at closing on the sale. Others use a bridge loan specifically designed for this scenario. Both have costs and trade-offs, and not every lender offers them on every property. If you’re considering buying first, that conversation with your lender should happen before you start touring homes.

For a real example of how this plays out, I wrote up a recent client story: How a Bridge Loan Let My Buyers Win the Home Before Selling Theirs — they found the one on its second day on the market, the seller wouldn’t take a contingency, and a bridge loan is what let them compete anyway.

Option 3: Make Your Offer Contingent on Selling Your Home

A home sale contingency is the middle path.

The National Association of REALTORS® describes a home-close contingency as one that gives buyers who already have a contract on their current home time to close on that sale before purchasing the next home. In plain English: your purchase of the next home depends on your current sale working out.

That protects you as the buyer. But it can also make your offer less attractive to the seller, because your offer now depends on a transaction they don’t control.

In Tennessee, you’ll typically see this structured in one of two ways:

- Contingent on closing. Your current home is already under contract; you just need it to actually close before you can close on the new one.

- Contingent on sale. Your current home isn’t under contract yet, and you need to find a buyer first. This is the weaker version.

A contingent offer is more workable when:

- Your current home is already listed

- Your current home is already under contract

- Your buyer’s inspection and appraisal have already cleared

- The home you want has been sitting longer (40+ days on market is a different conversation than 5 days)

- The seller has fewer competing offers

- You can offer strong terms in other areas — clean financing, flexible closing, higher earnest money, no other contingencies

In today’s more balanced Middle Tennessee market, contingent offers have more room than they did at the peak. They’re still not the strongest offer type — they probably never will be — but they’re not the automatic rejection they once were either. Especially on homes that have been on the market for a while, a clean contingent offer with a credible plan can win.

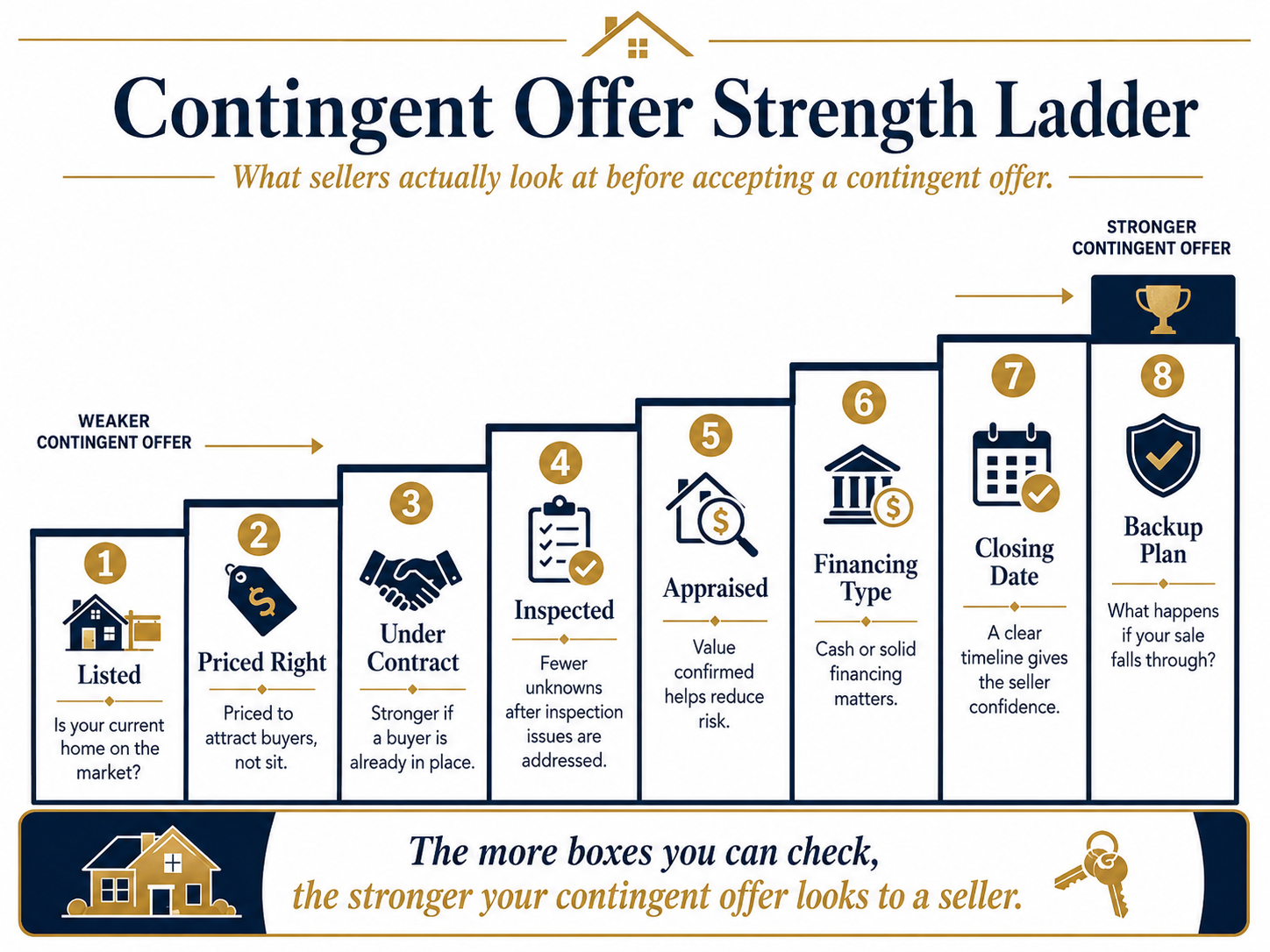

What Sellers Actually Look at on a Contingent Offer

If you’re going to make a contingent offer, understand how the listing side will evaluate it.

A seller isn’t just looking at your price. They’re looking at certainty. Specifically:

- Is your current home already listed?

- Is it priced correctly for current local comps?

- Is it under contract? Cash or financed?

- Has the inspection happened? Were there any issues?

- Has the appraisal happened? Did it hit?

- Is your buyer using financing? What loan type? Pre-approved or pre-underwritten?

- When is your current closing date?

- What’s your backup plan if your sale falls apart?

The further along your current sale is, the more comfortable a seller will be with your contingency. A buyer whose current home is under contract, inspected, appraised, and three weeks from closing looks completely different from a buyer who hasn’t even listed yet.

When I write a contingent offer for a client, the cover page essentially answers all of those questions before the listing agent has to ask. That presentation matters — and it’s part of what a buyer’s agent should be doing on your behalf. (For more on that side of the equation, see last week’s post: Do I Need a Real Estate Agent When Buying New Construction in Middle Tennessee?.)

The Middle Tennessee Factor

Local market conditions matter — and they vary more than people think across the towns I cover.

A home in Hendersonville behaves differently than a home in Portland. A well-priced subdivision home in White House moves faster than a rural property with acreage in Robertson County. A newer build in Gallatin competes directly with builder inventory and incentives. A unique property in Cottontown might have fewer direct comps but still attract a specific buyer pool willing to pay for it.

That’s why national advice on “sell first vs. buy first” only gets you so far. The right strategy depends on:

- Your specific home’s marketability. Lot, layout, condition, school zone, price band.

- The price band you’re moving into. Buying at $450K is a different market than buying at $850K.

- The competition where you’re moving. Are you competing with builder inventory? Cash investors? Out-of-state relocation buyers with corporate packages?

- Your timeline flexibility. A military move with a hard date is a different problem than a downsizer with no deadline.

More inventory across the region generally helps you as a buyer — more options, less pressure. But the same inventory affects you as a seller, because your home needs sharper pricing, better preparation, and stronger marketing to stand out. Greater Nashville REALTORS® has described the current shift as one where buyers gain choice and sellers have to adjust to a more balanced market. That’s the same shift, viewed from two sides of your transaction.

For the local numbers behind the towns above, the ZIP-level reports I publish are built for exactly this — White House 37188, Portland 37148, Gallatin 37066, Cottontown 37048, and the broader Robertson County and Sumner County reports.

My Practical Recommendation

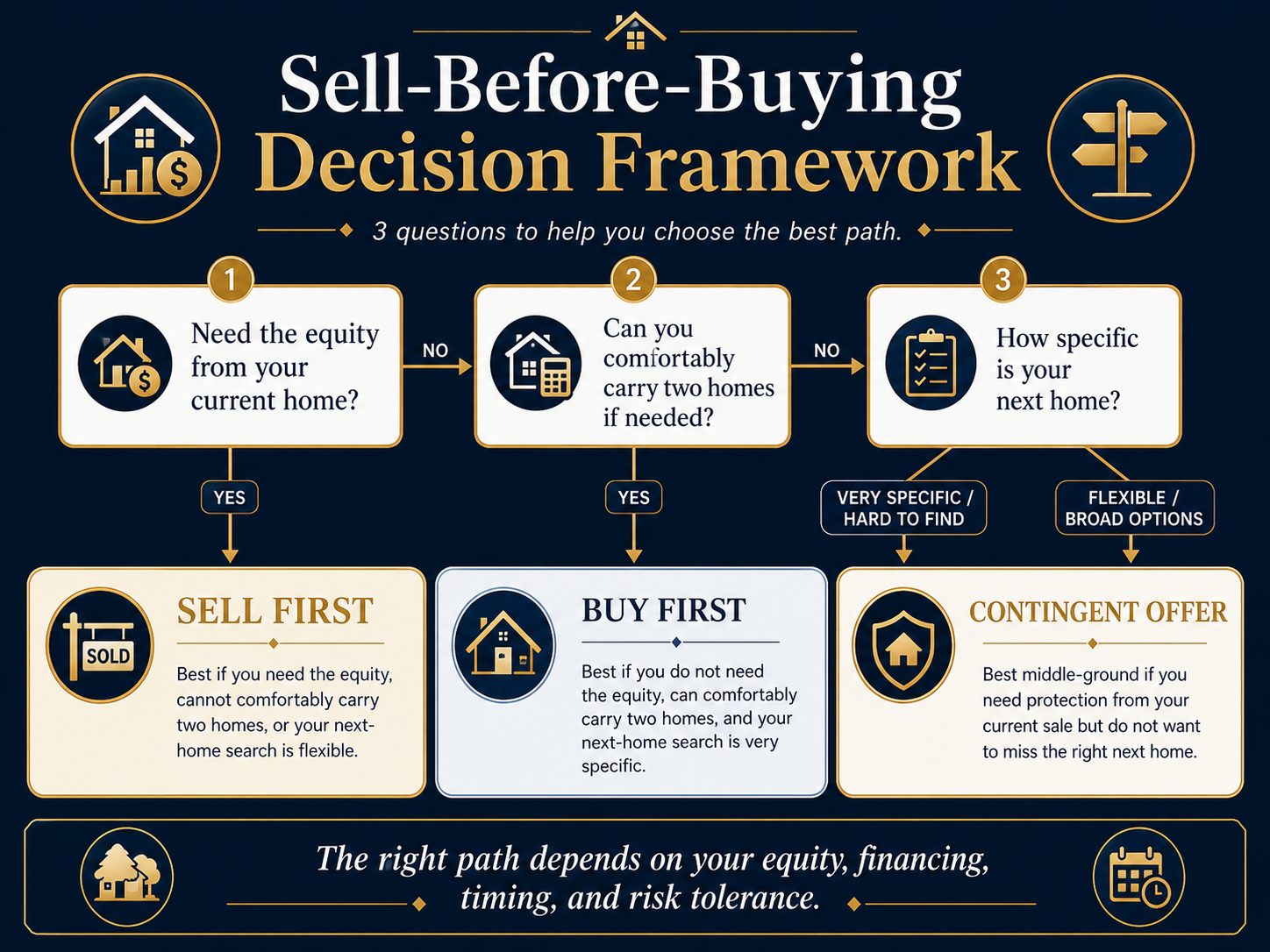

If you’re buying and selling at the same time, I’d start with three honest questions:

1. Do you need the equity from your current home to buy the next one? If yes, selling first or using a contingency is usually the safer path. Buying first only works if you have other liquidity — cash, a HELOC, family help, or a lender willing to underwrite both properties.

2. Can you comfortably carry two homes if the sale takes longer than expected? “Comfortably” means without financial stress, not “technically able to.” If the answer is no, buying first creates risk that compounds the longer your home sits.

3. How hard will it be to find your next home? If your next home needs to be very specific — one-level living, a certain school zone, acreage, a workshop, a specific community — your search may take longer than your sale. That changes the math.

For most Middle Tennessee homeowners I work with, the best plan isn’t pure “sell first” or pure “buy first.” It’s a sequenced plan that lines up:

- Pricing and prepping your current home with real comps (not a wishful estimate)

- Talking to a lender about both scenarios before you list anything

- Studying the target market for your next home — and being honest about how long that search may take

- Knowing in advance what you’ll do if either side stalls

Done well, this turns a stressful, high-stakes move into a sequence of decisions you’ve already thought through. Done poorly — or under time pressure — it becomes the kind of move you remember for the wrong reasons.

Bottom Line

Selling first gives you more financial certainty. Buying first gives you more convenience and control. A home sale contingency connects the two, but it usually weakens your offer relative to non-contingent buyers.

The right move depends on your equity, your financing, your current home’s marketability, and the type of home you’re trying to buy.

If you’re moving within Middle Tennessee or relocating to the north-of-Nashville area, the smartest approach is to plan both transactions together instead of treating the sale and purchase as separate decisions. They’re not separate. The way one goes will affect the other every step of the way.

If you want help walking through your specific situation — the equity math, the timing, what your current home is actually worth, and what’s realistic in the price band you’re moving into — that’s the conversation I have all day. You can book a consult, reach me at (615) 491-1638, or read more about how I work with buyers and how I help sellers.

Sources: NAR Consumer Guide: Real Estate Sales Contract Contingencies, Greater Nashville REALTORS® Market Data Monthly, Freddie Mac Primary Mortgage Market Survey.