They’d waited two years for the right house. When it finally showed up — on day two, before they’d sold their own — the seller wouldn’t take a contingency. Here’s how a bridge loan let them win it anyway.

For a lot of homeowners, one question is the thing standing between them and a move they really want to make:

What do you do when you find the perfect home before you’ve sold yours?

You love where you’d go next — but your money is tied up in the house you’re living in, and you can’t exactly write an offer with “as soon as mine sells” stapled to the front of it.

I just helped a couple work through exactly this, and the way we solved it is worth sharing — because it’s an option a lot of buyers north of Nashville don’t know they have.

Two years of waiting for the right one

I’d been working with these clients for a couple of years. They weren’t in a hurry, and they weren’t going to settle. They knew what they wanted, and they were willing to wait for it — which, honestly, is the kind of buyer who deserves to get the house when it finally shows up.

So when the right one hit the market, I wasn’t going to let them miss it.

We were standing in it on its second day on the market. They loved it — the real kind of loved it, not the talk-yourself-into-it kind. This was the one we’d been waiting for.

The problem: they already owned a home

Here’s where it gets complicated, and where a lot of buyers get stuck.

My clients already owned a home. Most people in that position assume the move is: sell first, then buy. Or they try to write an offer with a home sale contingency — meaning “we’ll buy yours once ours sells.” I broke down all three of those paths a few weeks ago in Should I Sell My Current Home Before Buying Another One? — this story is what happens when the textbook answer runs into a real listing.

So I did what I’d do for any client: I asked the listing agent whether the sellers would entertain a home sale contingency.

They wouldn’t. And honestly, I didn’t blame them. The house had just come on the market. It was far too early for a seller to tie up their brand-new listing waiting on someone else’s house to sell. A contingent offer that early is just a weaker offer, and a fresh listing has no reason to accept a weaker offer.

That’s the wall a lot of buyers hit — and where the conversation usually ends with “well, guess we’ll keep looking.”

It didn’t have to end there.

The solution: a bridge loan

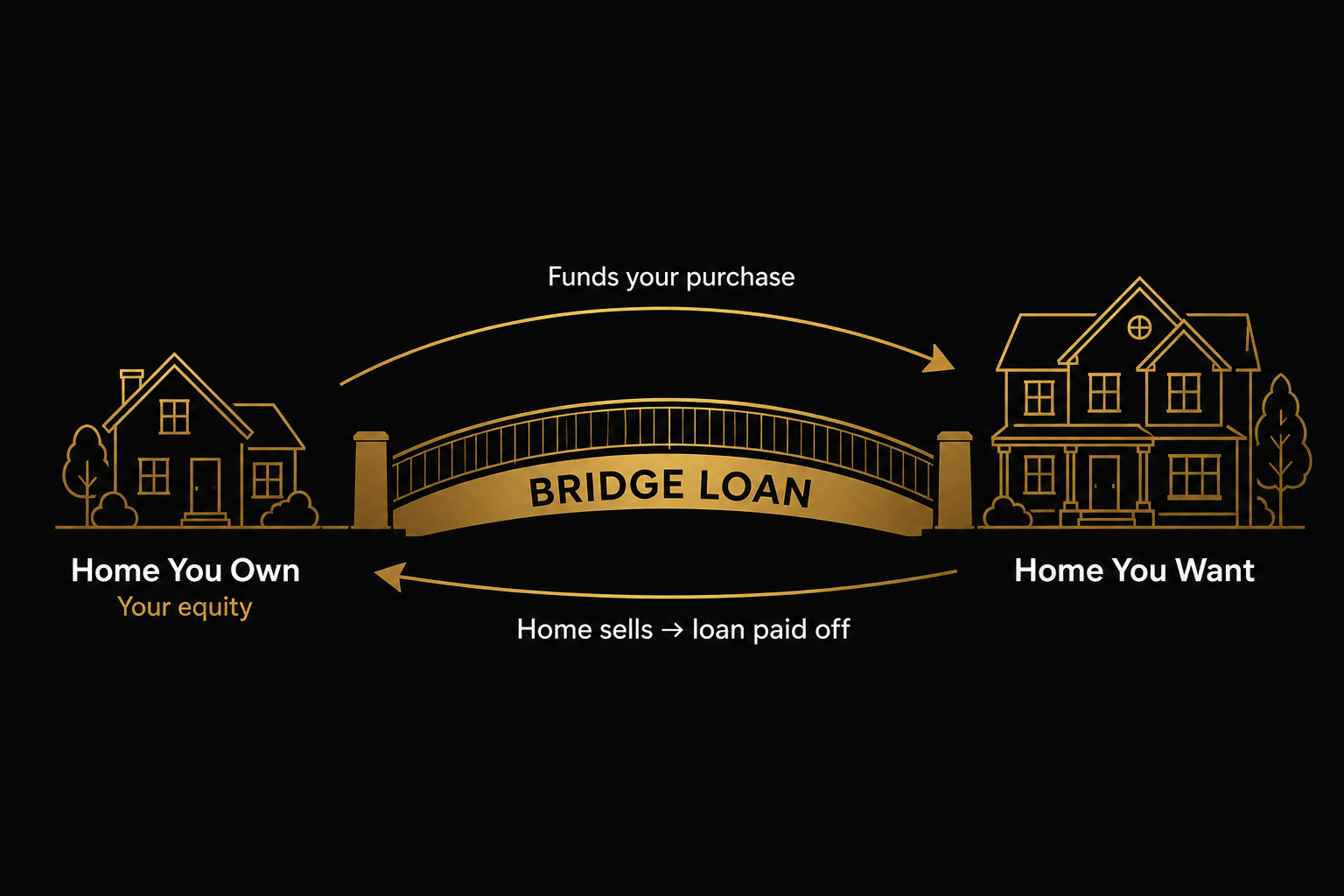

I told my clients there was another path. They could go ahead and buy the house they loved — without selling theirs first, and without a contingency — by using a bridge loan.

A bridge loan is short-term financing that lets you tap the equity in the home you already own to fund the purchase of your next one. It “bridges” the gap between buying the new home and selling the old one. When your current home sells, the bridge loan gets paid off.

The big advantage is what it does to your offer. Instead of “we’ll buy this once our house sells,” you get to make a clean, non-contingent offer — the kind a seller actually wants to see. You compete like a buyer who doesn’t have a house to sell, because for the purposes of the offer, you don’t.

In a more balanced Middle Tennessee market, that strength still matters. Inventory is higher than it was during the frenzy years and sellers are negotiating again — but on a brand-new listing that everyone wants, a clean offer is still what wins. A bridge loan is one way to be that clean offer when you already own a home.

How it played out

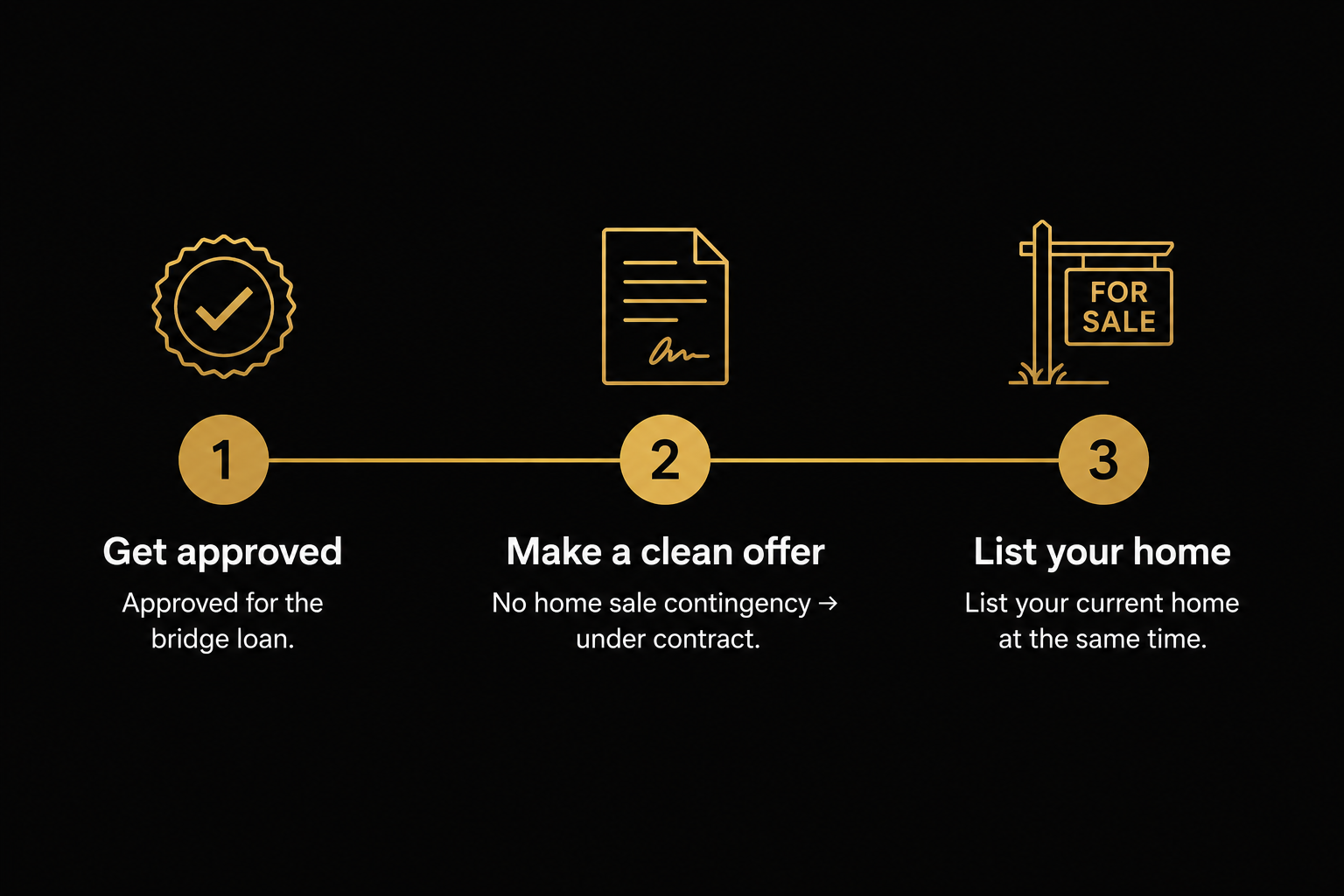

We moved fast and in the right order:

- My clients got approved for the bridge loan.

- We wrote the offer on the home they loved — clean, no home sale contingency — and got it under contract.

- We listed their current home at the same time.

That last part matters. The bridge loan isn’t a reason to sit on your old house — it’s the thing that buys you the breathing room to sell it the right way instead of in a panic. We got their home on the market right behind the purchase, so both sides of the move were moving together.

A clean offer doesn’t mean an unprotected one

Here’s a piece people misunderstand about “strong offers”: a clean offer doesn’t mean you throw away every protection. It means you strip out the contingency the seller is afraid of — and keep the ones that protect you from a real risk.

This particular couple was in an unusually strong spot. They owned their current home outright — no mortgage, lots of equity. That mattered for two reasons. First, it’s exactly the situation a bridge loan is built for: there was real equity to bridge against. Second, it let us strengthen the offer in a way most buyers can’t.

Because their finances didn’t depend on a new loan going through, we were able to waive the financing contingency — the clause that lets a buyer walk if their mortgage falls apart. To a seller, waiving that is a big deal: it removes one of the main ways a deal dies.

But we did not waive the protections that guard against an actual mistake:

- We kept the appraisal contingency, so they couldn’t get stuck overpaying above what the home is actually worth.

- We kept the inspection, so they knew exactly what they were buying before they were locked in.

That’s the balance. We gave the seller the certainty they wanted by removing the contingency they worried about, while keeping the two safeguards that protect the buyer from overpaying or buying a problem. A strong offer and a smart offer aren’t opposites.

One important caveat: waiving the financing contingency only made sense because of their specific situation — outright ownership and deep equity. For a buyer who needs the new mortgage to close, waiving financing is a real risk, not a flex. This is exactly the kind of thing you decide case by case, with your agent and lender, based on your actual numbers — not because a blog told you “waive contingencies to win.”

Is a bridge loan right for everyone? No.

I’d be doing you a disservice if I made it sound free. A bridge loan is a tool, not magic, and it comes with trade-offs:

- It’s short-term, and the rate and fees are usually higher than a regular mortgage.

- You may be carrying two properties for a stretch while your current home sells.

- It works best when you have solid equity in your current home and it’s likely to sell in a reasonable window.

For the right buyer — someone with real equity, a home that will sell, and a “this is the one” property they can’t risk losing — it can be exactly the right move. For someone else, selling first, a HELOC, or a different structure might make more sense. Every situation is different, and the actual terms come from your lender, not from a blog post.

This is also the “contingent-vs-bridge” decision I promised was worth its own conversation back in Should I Wait for Mortgage Rates to Drop?. For these clients, the bridge made sense. For the next buyer, it might not — and that’s the whole point of talking it through before you fall in love with a listing.

The takeaway

If you already own a home and you’ve been telling yourself you can’t go after the next one until yours sells — that’s not always true. The order isn’t fixed. With the right financing and the right plan, you can buy the home you love and sell yours on a smart timeline instead of a desperate one.

That’s the part I love about this work: it’s rarely “you can’t.” It’s usually “here’s how.”

If you’re a homeowner in White House, Gallatin, Hendersonville, Portland, or anywhere in the Middle Tennessee area thinking about a move and you’re not sure how to make the timing work, that’s exactly the kind of puzzle I like to solve. Let’s talk through your options before you decide you have to wait. You can book a consult, reach me at (615) 491-1638, or read more about how I work with buyers and how I help sellers.

This post is for general education and isn’t financial or lending advice. Loan availability, terms, and what makes sense for your situation depend on your lender and your specific circumstances.

Sources: Investopedia — Bridge Loan, Consumer Financial Protection Bureau — Buying a House, NAR Consumer Guide: Real Estate Sales Contract Contingencies.